My early retirement decision was made based on The 4% Rule.

If you have a million dollars and you can safely live on $40,000, then you can retire.

You can think of it as the 25x rule as well. If you need $100,000 a year, then you should have $2.5 Million at your disposal.

The rule does take inflation into account. But recent years have put stress on that assumption.

The Data

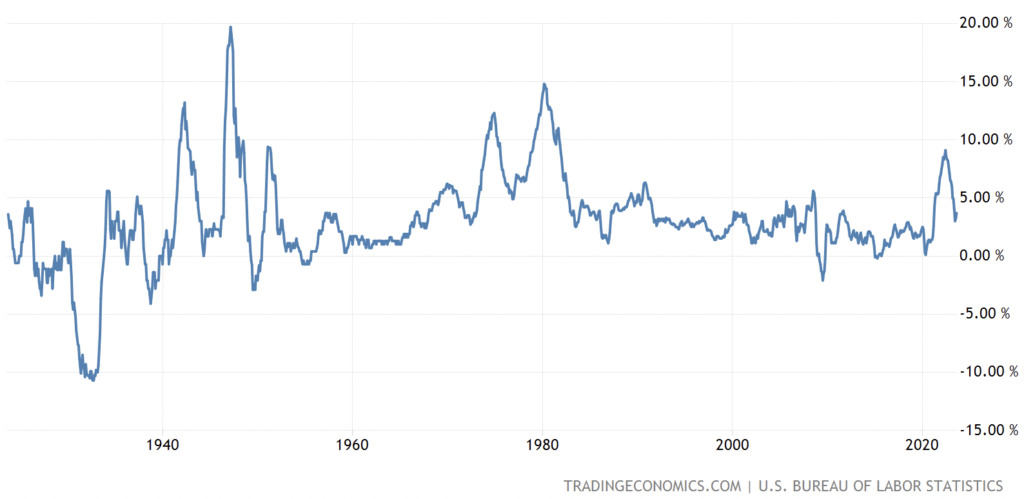

For the first 38 years of my life, inflation was ~2.5%.

Interest rates have been a different story. Around my birth, they went on a rollercoaster to the bottom.

Finally, the stock market has been strong. But there have been bear periods that could wreck your investments.

For 1960-2022, here are the annual averages:

| Interest Rates | 4.79% |

| S&P 500 | 11.23% |

| Inflation | 3.76% |

If you put all your cash into a savings account, you would grow your money at 1% annually... on average.

If you put your money in an S&P 500 Fund, you would grow your money at 7.5% each year... on average.

There are no guarantees with averages.

In 2022, inflation was 8.3%, S&P 500 returned -18.1% and the average interest rate was 1.7%. No matter where you turned, you were losing money.

2022 Hypothetical

Imagine it is January 1, 2022. You have $1 Million and live off of $40,000/year. You're young, so you have an 80/20 stocks/cash ratio.

Come January 1, 2023, your $800K in stocks is worth $655,200. Your $200K in cash/bonds is worth $203,400.

Your $1 Million assets are now only worth $818,600.

You didn't just "lose" $181,400. With high inflation, you would need to live off $43,320 in 2023—you need $1,083,000.

You are now $264,400 behind.

As of 2023, inflation is 3.7%, the S&P 500 has returned 16%, and the average interest rate is 5%.

At the end of 2024, You would have $759,661 in stocks and $171,906 in cash. After your living expenses, you now have $888,247. You now need to live off $44,923 in 2024 (a 12.3% increase in only two years). You need $1,123,071.

Even after a terrific market year, where your total assets are up almost $70K, you are still $234,824 behind.

So What?

You need to know the current economic conditions to understand if you can still retire.

General inflation is one of many things you need to monitor. Are you still able to live off the amount you have been? Is your food and housing budget keeping steady with inflation, or has your spending outpaced it?

Stay smart. Stay retired.